Feb 6, 2026

How to wind up a company: A Practical, Click-Worthy Guide

Winding up a company is the formal process of calling time on the business. It’s about methodically closing down operations, selling off what you own, settling up with everyone you owe, and then, if there’s anything left, distributing it to the shareholders. It's not a decision to take lightly; it involves legal steps that bring the business's existence to a permanent close.

Is It Time to Close the Doors?

Deciding when to shut down your business is probably one of the toughest calls a founder will ever have to make. It can feel like a personal failure, but it’s vital to see it for what it is: a strategic business decision. The real goal here is to act decisively, protecting your personal assets and freeing up your time and capital before things spiral into a forced, messy closure.

This isn’t just about having a bad quarter or a negative balance sheet. It’s a moment for a hard, objective look at the financial, operational, and even personal signs telling you that the road ahead is a dead end. One of the most common mistakes I see is founders waiting too long, which can dramatically increase personal liability and slam the door on better exit options.

To help you assess your own situation, here’s a quick reference table outlining the common warning signs.

Key Indicators It Might Be Time to Close Your Company

Financial Indicators | Operational Indicators | Personal Indicators |

|---|---|---|

Persistent Cash Flow Issues: Consistently struggling to pay suppliers, rent, or staff. | Insurmountable Market Shifts: Your core product or service is becoming obsolete due to new tech or changing consumer habits. | Founder Burnout: Chronic stress, exhaustion, and a complete loss of passion for the business. |

Heavy Debt Reliance: Taking on new loans just to service existing debt; caught in a debt spiral. | Loss of Key Talent: Critical team members are leaving, and you can't attract or afford replacements. | Dipping into Personal Finances: Using personal savings or credit to keep the business afloat with no clear end in sight. |

Inability to Secure Funding: Investors and lenders are no longer willing to back the company. | Supply Chain Breakdowns: Constant, unsolvable problems with getting the materials or services you need. | Loss of Belief: You no longer believe in the company’s mission or its potential for success. |

Declining Profit Margins: Squeezed by rising costs and falling prices with no way to reverse the trend. | Losing to Competitors: Consistently being outmanoeuvred or out-innovated by rivals in the market. | Health Impacts: The stress of running the business is negatively affecting your mental or physical health. |

If you find yourself ticking multiple boxes in this table, it's a strong signal that you need to seriously evaluate winding up the company as a strategic option, not a last resort.

Financial Red Flags

A constant lack of cash is the most glaring warning sign. If your business is in a perpetual state of scrambling to pay suppliers, meet payroll, or cover the rent, you’re looking at a symptom of a much deeper problem. We’re not talking about a single slow month; this is a relentless pattern of just about getting by.

Another massive red flag is when the company is leaning heavily on debt simply to keep the lights on. If you're borrowing money just to pay off other loans, you're likely caught in a debt spiral – a situation that is notoriously difficult to break free from.

Let's be realistic about the UK business climate. The latest data is pretty sobering, showing that company insolvencies are at near-record levels. In the last year, roughly one in every 187 active companies has gone into a formal insolvency procedure. This isn't a coincidence; it's a direct result of high interest rates and soaring operational costs.

Operational and Market Pressures

Sometimes, the books look okay, but the world outside your door has changed. A fundamental market shift—like a new technology that makes your flagship product redundant or a sudden pivot in consumer behaviour—can knee-cap even a healthy business. If your market has fundamentally moved on and your attempts to pivot haven't worked, it’s probably time for a rethink.

A slow, grinding operational decline can be just as fatal. This might show up as losing key people you simply can't replace, your supply chain becoming unreliable, or just being unable to innovate fast enough to keep pace with competitors. When the day-to-day running of the business feels like a constant battle, it's a good sign the model is broken. It's worth exploring the various scenarios that lead other founders to this same difficult crossroad.

The Personal Toll on Founders

Finally, we have to talk about the human cost. Founder burnout is a very real, and very valid, reason to consider winding down. When the passion that got you started has been replaced by crippling stress, exhaustion, and a genuine loss of faith in the future, your ability to lead effectively is compromised.

Continuing to pour your energy, health, and personal savings into a venture that's no longer viable is a direct path to personal and financial ruin. Knowing when to stop isn't failure; it's a mark of strength and good judgment that allows you to close one chapter properly and prepare for whatever comes next.

Choosing Your Liquidation Route: Solvent vs. Insolvent

Once you’ve made the difficult call to close up shop, the next move is probably the most important one: taking a brutally honest look at your company’s finances. This isn't just an accounting exercise; it's a legal crossroads that will dictate the entire process. You're essentially figuring out if you're closing a healthy business or one that's run out of road.

The core question is one of solvency. A company is legally solvent if its assets are worth more than all its liabilities, including any potential future debts. On the other hand, if you can't pay your bills as they come due, or your debts outweigh your assets, the company is legally insolvent. There's no grey area here, and getting this right is paramount.

The Solvent Path: A Members’ Voluntary Liquidation (MVL)

Let's say your company has served its purpose. Maybe you're retiring, or a project has concluded, and you're left with a healthy balance sheet. In this case, the standard and most tax-efficient route is a Members’ Voluntary Liquidation (MVL).

An MVL is a formal process driven by the directors to close a solvent business down properly. Its main draw is how the remaining funds are paid out to shareholders. Instead of being taxed as income, they're treated as capital distributions.

This often opens the door to significant tax relief:

Business Asset Disposal Relief (BADR): This used to be called Entrepreneurs' Relief. It can slash your Capital Gains Tax rate to a mere 10% on qualifying assets.

An Orderly Closure: Everything is managed by a licensed insolvency practitioner, ensuring a clean and structured sale of assets and distribution of the proceeds.

Think of an MVL as a strategic exit. It’s the cleanest, most professional way to extract the value you’ve worked hard to build, ensuring you and your fellow shareholders get the best possible return while formally settling things with HMRC and Companies House.

The Insolvent Path: A Creditors’ Voluntary Liquidation (CVL)

The picture changes entirely when a company’s debts are greater than its assets. From the moment you realise this, your legal duties as a director pivot. You're no longer just responsible to the shareholders; your primary duty is now to the company's creditors. Continuing to trade while knowingly insolvent can have serious consequences, including personal liability.

In this situation, the most common path is a Creditors’ Voluntary Liquidation (CVL). While the name might sound like it’s forced upon you, a CVL is actually started by the directors themselves when they accept the business can no longer continue.

Taking this step is far more common than you might think. In fact, official statistics show CVLs are the most frequent type of corporate insolvency in the UK, making up around 78% of all formal procedures in England and Wales. This tells us that most directors choose to take control of a bad situation rather than waiting for a creditor to force their hand with a winding-up petition.

With a CVL, you appoint a licensed insolvency practitioner who takes over. They sell off the company's assets and pay the creditors in a legally defined order. Crucially, this process protects directors from accusations of wrongful trading, as long as they act responsibly as soon as they identify the insolvency.

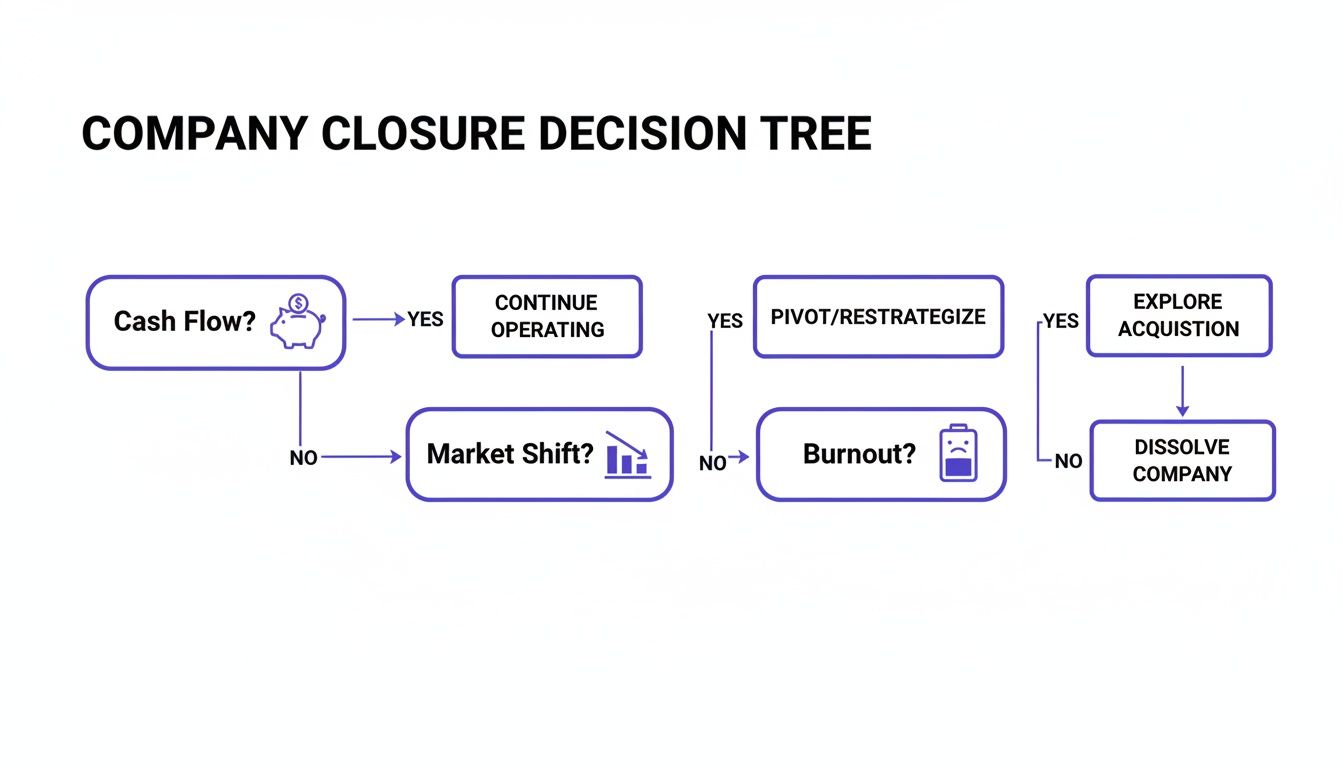

This decision tree can help you visualise the triggers that often lead a business owner down one of these paths.

As the graphic shows, things like persistent negative cash flow, a fundamental shift in the market, or sheer founder burnout are often the catalysts that force this decision.

Choosing the right liquidation route is absolutely critical, as a misstep can have serious legal and financial repercussions. An unflinching review of your balance sheet is the non-negotiable first step. You can also see a direct comparison of different closure options to get a clearer picture of the details.

Getting the Paperwork and Legal Steps Right

Let’s be honest, the administrative side of closing a company can feel like a minefield of legal jargon and endless forms. It’s easy to feel overwhelmed, but if you break it down into a series of clear, manageable actions, you can stay in control and make sure everything is done by the book.

The process kicks off with making the decision official internally. This isn't just a quick chat; it's a sequence of formal, documented steps that create a legal paper trail. It starts with the directors holding a board meeting to pass a resolution that recommends winding up the company.

Once the board has agreed, you need to call a general meeting for the shareholders. Here, they'll vote on a special resolution to put the company into liquidation and formally appoint a licensed insolvency practitioner. To get this over the line, you’ll need a thumbs-up from at least 75% of the voting shareholders.

The Key Documents You'll Need to Handle

The paperwork you'll face depends entirely on whether your company is solvent or insolvent. Getting your head around these key documents is vital, as they form the legal foundation of the whole process. Each one has a specific job and carries significant legal weight.

For a solvent closure, known as a Members’ Voluntary Liquidation (MVL), the star of the show is the Declaration of Solvency. This is a sworn statement, signed by most of the directors, confirming you’ve thoroughly reviewed the company's finances and are confident it can pay all its debts in full within 12 months.

Don't take this document lightly. Signing a false declaration without having good reason to believe it's true is a criminal offence. It has to be backed up by a detailed Statement of Assets and Liabilities that proves the company is in good financial health.

On the other hand, if you're dealing with an insolvent closure, or a Creditors' Voluntary Liquidation (CVL), the crucial document is the Statement of Affairs. This gives a complete snapshot of the company’s financial position at that specific moment, listing every asset and liability. It’s prepared for the creditors, giving them a clear picture of the situation and what they can realistically expect to get back.

Who You Need on Your Team

You're absolutely not expected to navigate this legal maze by yourself. Bringing in the right professionals isn't a luxury; it’s a necessity to ensure a smooth, compliant closure and protect yourself from costly mistakes or even personal liability.

The most important person you'll work with is a Licensed Insolvency Practitioner (IP). You are legally required to appoint an IP for both solvent and insolvent liquidations. They effectively take control of the company, manage the sale of assets, liaise with creditors, and make sure every statutory duty is fulfilled. Your accountant is also a key player, especially for preparing final accounts, sorting out final tax liabilities like Corporation Tax and VAT, and ensuring all the necessary filings with HMRC are spot on.

A Practical Winding-Up Checklist

To keep things moving and ensure nothing gets missed, it helps to follow a clear roadmap. This checklist covers the main tasks you'll need to tick off, from the first filings right through to the company's final removal from the register.

Official Filings: Your IP will handle the bulk of the filings with Companies House, like submitting the shareholder resolutions and registering their own appointment. They’ll also publish the required legal notices in The Gazette.

Tax Obligations: Make sure the final VAT and Corporation Tax returns are filed with HMRC and any outstanding PAYE is settled. The taxman needs to be completely satisfied before the company can be closed for good.

Employee Duties: If you have staff, you must follow the correct redundancy procedures. This means giving proper notice and making sure they receive their final wages and any redundancy pay they're entitled to.

Keeping Stakeholders in the Loop: You need to tell everyone who matters that the company is closing down. This includes your bank, insurers, suppliers, and customers.

Final Deregistration: After all the assets have been sold, creditors have been paid, and any remaining funds distributed to shareholders, the IP will apply to have the company struck off the register at Companies House. At that point, it officially ceases to exist.

Managing this entire sequence requires real care and attention to detail. If you're just beginning to explore your options, our guide on getting started with the company closure process provides some more foundational knowledge to help you on your way.

An Alternative Route: Liquidation Via Sale

For most entrepreneurs, the idea of a standard liquidation is a real headache. It often feels slow, overly formal, and painfully public, sometimes dragging on for months—or even years—while you're still legally tied to a venture that's run its course.

But what if there was another way? A path to a clean, fast, and final exit?

This is where a clever model known as Liquidation Via Sale comes into the picture. It’s a strategic off-ramp for founders who want to skip the drawn-out stress of a conventional winding-up process and get on with their next project, free and clear.

How Liquidation Via Sale Works

The concept itself is surprisingly simple. Instead of you overseeing the entire liquidation, you sell 100% of your company's shares to a specialised firm. The price is nominal—often as little as £1—and the deal is structured as a standard share purchase agreement, making it a perfectly routine and legal business transaction.

Once the sale goes through, the specialist firm takes over completely. They appoint their own director, and your name is removed from the company register, usually in just a few business days. From that point on, you are officially and legally disconnected from the company. The new owner then assumes all the responsibility for managing the final winding-down process, making sure everything is handled in full compliance with local laws.

The real magic is the immediate finality. Your legal ties are severed in days, not months or years. All communication from creditors, tax authorities, and anyone else is redirected to the new director, giving you a complete and clean break.

Who Is This For?

This approach isn't for everyone, but it’s a perfect fit for certain situations where speed and a clean exit are what matter most. It’s particularly useful for:

Founders of Failed Startups: Entrepreneurs whose ventures didn’t pan out and who need to close the book quickly to focus on their next big idea, without the baggage of a long liquidation.

Non-Resident Owners: People who own a UK-based company but live elsewhere. This is an invaluable tool for a remote, hassle-free exit without having to travel or deal with unfamiliar bureaucracy.

Dormant Company Owners: If you have a limited company that’s no longer trading but is still racking up admin costs and filing obligations, this is a swift way to shut it down for good.

Directors Under Creditor Pressure: For businesses facing a constant barrage from creditors, this method can stop the stressful calls and letters almost overnight by transferring that burden to the new owner.

Comparing the Two Paths

When you look at this modern approach next to a traditional liquidation, the difference is night and day. A standard winding-up process leaves the burden of management, communication, and legal compliance on your shoulders for a long time. Liquidation-via-sale, on the other hand, transfers that burden away from you entirely.

To really see the difference, let’s put them side-by-side.

Traditional Liquidation vs Liquidation Via Sale: A Comparison

The table below breaks down the key distinctions between the two routes, highlighting how they differ in terms of time, effort, and outcome for you as the founder.

Feature | Traditional Liquidation (CVL/MVL) | Liquidation-Via-Sale |

|---|---|---|

Timeline | 6–24+ months until finalised. | Director removed in 3–30 days. |

Founder Involvement | High. You remain involved, liaising with the liquidator and creditors. | Minimal. Your involvement ends once the shares are sold. |

Creditor Communication | You and your liquidator handle all creditor contact. | Ceases immediately for you; handled by the new owner. |

Publicity | The liquidation is publicly announced in official gazettes. | The share sale is a private transaction. |

Control | You initiate the process but then cede control to a liquidator. | You control the decision to sell, then exit completely. |

Ultimately, your choice boils down to your priorities. If you need to manage a complex distribution of assets in a solvent company, a traditional Members' Voluntary Liquidation (MVL) might be the right call. But if your main goal is to quickly and legally distance yourself from a troubled or dormant company, a sale offers an unmatched blend of speed and peace of mind.

Common Mistakes to Avoid When Winding Up a Company

Closing down a company is a legal minefield. It’s a process where even a small misstep can land you in serious personal and financial trouble. Knowing where the common traps lie is the best way to get that clean break and move on without any legal ghosts following you.

When you’re under the immense pressure of a failing business, it’s easy to make errors in judgement. But these aren’t just admin slip-ups. Some mistakes can break through the "corporate veil," making you personally liable for the company's debts.

The path to winding up a company is full of potential pitfalls, but knowing what they are is half the battle. From mishandling debts to misjudging your legal duties, let's walk through the biggest mistakes I see directors make and how you can sidestep them.

Trading While Insolvent

This is, without a doubt, the most serious mistake you can make. The moment you realise (or frankly, should have realised) that your company can't pay its bills and there’s no realistic way back, your legal obligations pivot. Your primary duty is no longer to the shareholders; it’s to the company's creditors.

Carrying on trading and racking up more debt at this point is called wrongful trading. If the company ends up in liquidation, a court can make you personally responsible for all the debts built up from that point of insolvency. It's a classic case of chasing a miracle that almost never arrives, and the financial fallout can be devastating.

Making Preferential Payments

When you know the end is near, it’s tempting to pay off certain people first. Maybe it’s a friendly supplier you want to keep on good terms with, or a loan you've personally guaranteed. This is a huge red flag for a liquidator and is legally known as making a preferential payment.

You’re essentially putting one creditor in a better position than everyone else, which is a major no-no during insolvency. A liquidator has the authority to scrutinise every single transaction in the months before the company folded. If they spot a preferential payment, they can claw that money back and will certainly take a closer look at your actions as a director.

Your duty is to treat all creditors equally. Don't let personal relationships or pressure from one creditor push you into making a decision you'll regret. The principle of fairness is everything once insolvency looms.

Attempting to Hide or Sell Assets Cheaply

Another classic blunder is trying to shift company assets out of reach before the liquidator arrives. This could look like selling the company van to your brother-in-law for a tenner, or transferring the company’s intellectual property to another one of your businesses for free.

This is what's known as a transaction at an undervalue. A liquidator is legally required to investigate these kinds of deals and can go to court to have them reversed. Their job is to get the best possible return for all creditors, and deliberately gutting the company's value is a serious breach of your duties.

Ignoring Personal Guarantees

So many directors sign personal guarantees for business loans or leases without really thinking through the worst-case scenario. Well, when the company is wound up, those guarantees don't just vanish—they kick in.

The bank or landlord can, and almost certainly will, come after you personally for the money owed. One of the biggest mistakes is simply burying your head in the sand. You absolutely must:

List every personal guarantee you've signed.

Get a clear figure on exactly what you're liable for.

Get professional advice on your next steps, which could involve negotiating a settlement.

Ignoring a personal guarantee won't make it disappear. The only way to handle it is to face it head-on with a solid plan.

Got Questions About Winding Up a Company? We've Got Answers

Closing down a business isn't something you do every day, so it's natural to have a lot of questions. The whole process is tangled up with legal responsibilities and financial details that can feel overwhelming. Let's break down some of the most common queries we hear from directors who are at this crossroads.

How Long Does It Really Take to Wind Up a Company?

There's no single answer here – the timeline for shutting down a company can swing wildly depending on which path you take and how messy its affairs are.

If your company is solvent and you go for a Members' Voluntary Liquidation (MVL), you’re looking at the most straightforward route. Even so, it's not an overnight job. You should realistically budget for several months, and sometimes up to a year. The liquidator has to methodically sell off all the assets, pay off any lingering creditors, get the all-clear from HMRC, and only then can they distribute the final funds to the shareholders.

For an insolvent company, a Creditors' Voluntary Liquidation (CVL) is a different beast entirely. While the business usually stops trading almost immediately, the full liquidation process—selling assets and managing creditor claims—can easily take 12 to 24 months to wrap up completely.

A key alternative is the 'liquidation via sale' model, designed for speed. This process can see a director’s legal connection to the company severed in just a matter of days, completely bypassing the long, drawn-out timelines of traditional liquidation.

Can I Still Be a Director After My Company is Liquidated?

Absolutely. In the vast majority of cases, you can become a director of another company without any issues. Just because a business has closed, even an insolvent one through a CVL, it doesn't automatically bar you from future directorships.

The big "but" here is misconduct. If an investigation finds you've engaged in wrongful trading, fraud, or any other serious breach of your duties as a director, you could be disqualified for a period of 2 to 15 years.

Another crucial point to watch out for is the company name. The law is very strict about reusing a liquidated company's name or something very similar (under Section 216 of the Insolvency Act 1986). It’s designed to stop directors from just starting again with a clean slate while leaving old debts behind. If you get this wrong, you could be held personally liable for the new company's debts. Always get professional advice before you even think about it.

What Happens to Our Employees When the Company is Wound Up?

This is one of the toughest parts of the process. When a company is wound up, its business operations stop, which unfortunately means all employees are made redundant. Their employment contracts are legally terminated.

In an insolvent liquidation, your employees get a bit of protection—they are classed as preferential creditors. This puts them higher up the pecking order for payment from any company assets, ahead of unsecured creditors like your suppliers.

Their claims typically cover:

Unpaid wages (up to a certain limit)

Holiday pay they've earned but not taken

Some specific pension contributions

What if there's no money left in the company pot? Thankfully, employees aren't left high and dry. They can claim statutory payments from the government's National Insurance Fund. This covers redundancy pay, unpaid wages, and holiday pay. Your insolvency practitioner will give them all the forms and guidance they need to make a claim.

What's the Difference Between Winding Up and Striking Off?

This is a critical distinction, and getting it wrong can cause serious problems. Both options end with the company being removed from the Companies House register, but they are meant for completely different scenarios.

Striking off (or dissolution) is a simple, cheap way to close a company that is essentially a clean shell. It should have no assets, no liabilities, and has either never traded or has completely tied up all its loose ends. Think of it as an administrative tidy-up.

Winding up (or liquidation), on the other hand, is the formal legal process for a company that still has assets to sell and distribute, or debts that need to be settled. This process has to be handled by a licensed insolvency practitioner. Trying to strike off a company that owes money to HMRC or other creditors is a massive misstep. It can lead to the company being forcibly put back on the register, with directors facing an investigation and potentially being made personally liable for the debts.