Feb 8, 2026

Difference Between Bankruptcy and Liquidation for EU Founders

At first glance, bankruptcy and liquidation seem like two sides of the same coin, but they’re fundamentally different. Bankruptcy is a legal status — a court’s official recognition that a company is insolvent. Liquidation, however, is a process: the step-by-step procedure of winding down a company and selling off its assets to pay its debts.

A company can go through liquidation without ever being declared bankrupt, but a bankrupt company will almost always end up in liquidation.

Defining the Key Financial Endgames

When a business is in serious financial trouble, the words ‘bankruptcy’ and ‘liquidation’ start getting thrown around. For a founder facing this reality, knowing exactly what they mean is critical. They are two very different paths, with distinct triggers and outcomes, and confusing them can lead to costly errors and a lot of unnecessary personal stress.

Think of liquidation as the methodical process of closing a company for good. It involves selling everything the company owns—its assets—to pay back creditors as much as possible. If there's anything left over, it goes to the shareholders before the company is officially struck off the register. It's important to remember that liquidation isn't always a sign of failure. A perfectly healthy, profitable company might choose a voluntary liquidation if the owners simply want to close up shop and cash out.

Bankruptcy, on the other hand, isn't a process you choose; it's a legal declaration. It’s a court's formal acknowledgement that a company (or person) is insolvent, meaning it can no longer pay its bills. This legal status kicks off a range of protections and procedures, which might involve a court-supervised reorganisation to try and save the business, or it might lead directly to liquidation.

The crucial takeaway is this: Liquidation is an action (closing the company), while bankruptcy is a state (being legally insolvent). Liquidation can be a consequence of bankruptcy, but it can also be a strategic choice for a solvent business.

To make these initial ideas clearer, let’s break down the core differences.

Quick Comparison: Bankruptcy vs Liquidation

This table gives a high-level summary of the key distinctions between the legal state of bankruptcy and the process of liquidation. It helps to see them side-by-side.

Aspect | Bankruptcy | Liquidation |

|---|---|---|

Primary Definition | A legal status of being unable to pay debts. | The process of selling all assets to close a company. |

Core Purpose | To resolve insolvency under court protection, either through reorganisation or asset sale. | To formally end a company's existence and pay off its creditors. |

Typical Outcome | Can lead to company survival (reorganisation) or closure (liquidation). | Always results in the permanent closure of the company. |

Control | Often involves court-appointed trustees or administrators who oversee the process. | Can be voluntary (controlled by directors/shareholders) or compulsory (court-appointed liquidator). |

Ultimately, while both signal the end of a company's current form, bankruptcy is the court confirming the financial reality, whereas liquidation is the practical task of shutting everything down.

Diving Deeper: The Key Procedural Differences

While we've established the high-level distinction—bankruptcy is a legal status, liquidation is a process—the real divergence shows up in the nuts and bolts of how each unfolds. For any founder facing this crossroads, understanding these practical steps is everything. They dictate who’s in control, how long it will take, and what’s left at the end of the day.

The journey down either path starts with a specific trigger, and this is where they immediately split.

Triggers and Initiation: Choice vs. Crisis

Bankruptcy almost always kicks off because of insolvency—the simple, brutal fact that the company can't pay its bills. It's a reactive measure. More often than not, it's creditors who force the issue by filing a petition against the business when they're tired of waiting to be paid. A company can voluntarily file for bankruptcy, but doing so is a formal surrender to financial failure.

Liquidation, on the other hand, can be a deliberate choice or a forced outcome. A voluntary liquidation, especially what’s known as a Members’ Voluntary Liquidation (MVL), is often a strategic move by the directors and shareholders of a solvent company. Maybe they’re retiring, closing out a successful project, or just want to unlock accumulated profits in a tax-efficient way.

Of course, there's also compulsory liquidation, which looks a lot more like bankruptcy. This is when an insolvent company is forced to close by its creditors through a court order.

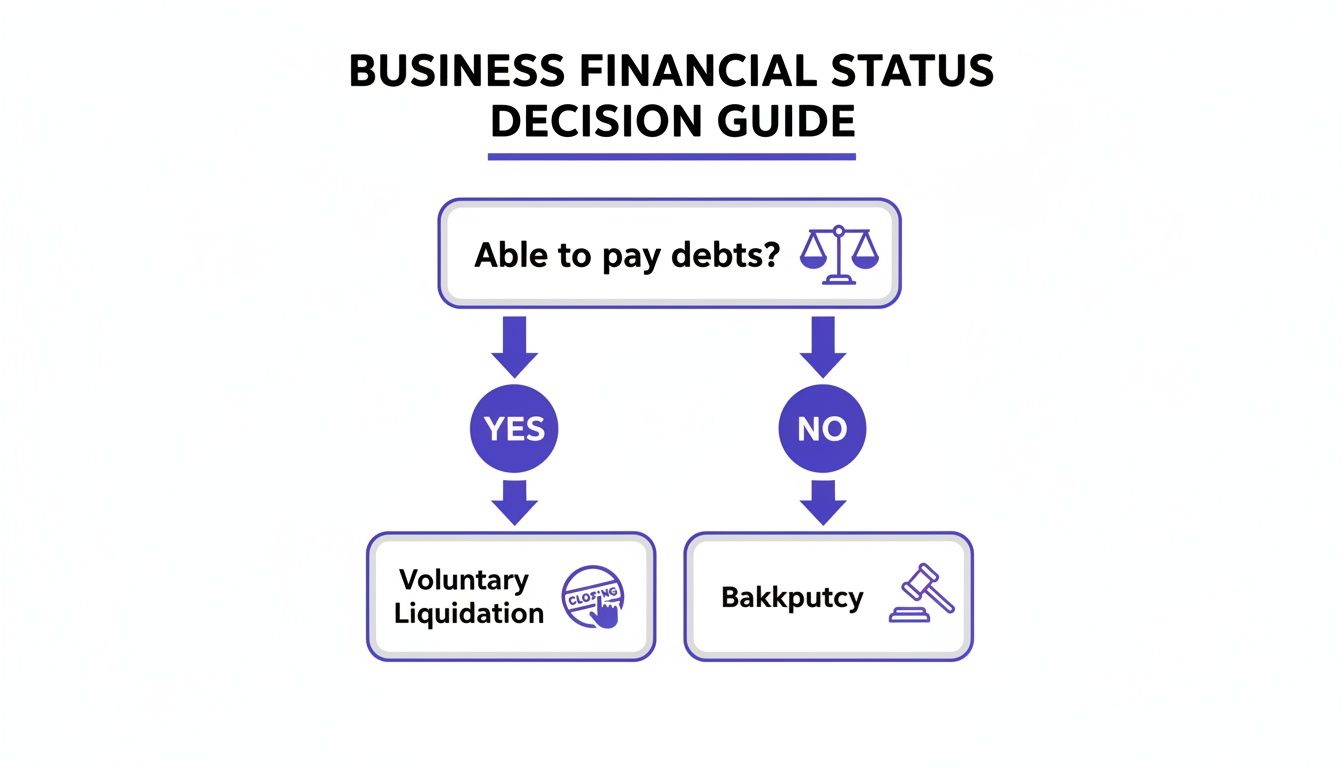

This flowchart maps out that critical decision point. It all comes down to whether you can pay your debts.

As you can see, solvency is the fork in the road. One direction leads to a planned, strategic closure; the other to a forced procedure driven by insolvency.

Legal Oversight and Control: Who's in Charge Now?

Once things get going, the level of outside control slapped on the company varies massively. Bankruptcy is an intense, court-supervised affair. A court-appointed trustee or administrator steps in and takes the reins of the company's assets and operations. The founder is effectively sidelined from day-to-day management. That trustee's job is to serve the creditors and the court, not the original owners.

Liquidation also brings in a professional, called a liquidator. Here's the key difference: in a voluntary liquidation, the directors and shareholders get to choose their liquidator, which means they keep a degree of influence over the process. In a compulsory liquidation, however, the court or creditors make the appointment, and just like in bankruptcy, the founder loses all control. For a step-by-step look at this, you can read our guide on how to wind up a company.

The biggest procedural difference really boils down to intent and outcome. Bankruptcy can be a lifeline, offering a path to survival through reorganisation. It’s a legal framework designed to restructure debt and keep the business breathing. Liquidation is always final. Its only purpose is to end the company’s existence.

Timelines and Complexity: Sprint vs. Marathon

The time it takes to get through these processes couldn't be more different. Bankruptcy, particularly a reorganisation, is a marathon. It can easily drag on for one to several years, filled with complex creditor negotiations, court hearings, and piles of reporting. The goal is to forge a viable plan for the future, and that just takes time.

Liquidation is usually much quicker, especially a voluntary one. A straightforward solvent liquidation can often be wrapped up in a few months to a year. It’s a much more linear process with one clear goal: sell assets, pay off debts, and shut the doors for good. Even a compulsory liquidation is typically faster than a complex bankruptcy reorganisation.

Core Goals: Reorganisation vs. Finality

Ultimately, all these procedural differences come back to their opposing goals. In the U.S., you see this clearly in the choice between Chapter 7 (liquidation) and Chapter 11 (reorganisation). For publicly traded firms, the choice is stark: roughly 80% of commercial bankruptcies are filed under Chapter 11, aiming to reorganise, while only 20% end in a Chapter 7 liquidation. This shows that bigger companies with valuable operations will fight tooth and nail to survive, whereas smaller businesses more often have to accept closure.

This principle is mirrored in the EU. A reorganisation-style bankruptcy is about salvaging the business as a going concern to preserve jobs and value. It provides a legal shield from creditors while the company tries to heal. Liquidation offers no shield and no second chances. It is the definitive end of the road—a clean, final closure that systematically dismantles the company. For any founder, grasping this finality is the most critical distinction of all.

The Fallout: What Happens to Owners, Creditors, and the Company?

Understanding the legal nuts and bolts of bankruptcy and liquidation is one thing, but the real gut punch comes from the consequences. The path you choose creates wildly different futures for the company's owners, its creditors, and the business itself. It’s not just a procedural choice; it’s a decision that defines the final chapter for everyone involved.

A Founder's Reality

For an entrepreneur, the most jarring change is the sudden loss of control. If you file for bankruptcy, especially a reorganisation, you're handing the keys over to a court-appointed trustee or administrator. You're no longer captaining the ship; your voice becomes one of many, often secondary to the court and the people you owe money to.

Liquidation offers a bit of a mixed bag. In a compulsory liquidation, you lose all control to a liquidator appointed by creditors or the court. It's over. However, in a Members' Voluntary Liquidation (MVL), which is for a solvent company, the owners actually keep a firm hand on the tiller, even getting to appoint the liquidator themselves.

And then there's personal liability. A limited company is supposed to be a shield, but it’s not indestructible. If you signed personal guarantees for business loans—and many founders do—your personal assets can be dragged into the mess in either scenario. Rest assured, both bankruptcy trustees and liquidators will dig deep into the directors' actions in the run-up to insolvency.

What many founders dread most is the hit to their reputation. Bankruptcy is a public admission of failure that can stick to an entrepreneur for years. While liquidation also signals an end, a voluntary wind-down of a solvent company can be framed as a strategic exit, keeping your reputation intact for whatever you decide to do next.

The Creditor's Point of View

For a creditor, it all boils down to two simple questions: How much of my money am I getting back, and when? The answers are starkly different depending on the process.

A bankruptcy reorganisation holds out the promise of a better recovery, but it’s a long game. The entire point is to keep the business alive so it can generate revenue to pay off debts over time. Creditors often get a say by voting on the reorganisation plan, which gives them a seat at the negotiating table.

Liquidation, on the other hand, is quick and dirty. The company's assets are sold off, often for pennies on the pound, and the money is paid out according to a rigid legal pecking order. If you’re an unsecured creditor, you’re at the very bottom of that list. The grim reality is that you’ll likely see very little, if anything. In the US, for example, over 95% of Chapter 7 liquidations are "no-asset" cases, which means unsecured creditors walk away with absolutely nothing.

Here’s how it breaks down for creditors:

Aspect | Bankruptcy (Reorganisation) | Liquidation |

|---|---|---|

Recovery Potential | Higher potential, but paid over time from future profits. | Lower, and strictly limited to what asset sales bring in. |

Timeline | A slow, drawn-out process. It can take years to see payments. | Much faster, but the payout is usually a fraction of the debt. |

Involvement | Creditors can often vote on the restructuring plan. | Minimal involvement beyond filing a formal claim. |

The Company's Ultimate Fate

This is where the two paths diverge completely. One offers a glimmer of hope for survival; the other is a guaranteed end.

Bankruptcy's Lifeline: A reorganisation is like sending the company to an intensive care unit. It gets legal protection—an "automatic stay"—from creditors, creating the breathing room needed to restructure its finances and debts. The goal is to emerge from the process as a more streamlined, viable business.

Liquidation's Finality: Liquidation is the company’s funeral. There is no coming back. The process is designed to dismantle the business, sell off every last asset, and scrub its name from the official register for good.

Making the right call means looking past the legal jargon and seeing these real-world outcomes clearly. By weighing these different scenarios, founders can choose a path that truly aligns with their financial, professional, and personal realities. To get a better sense of how these situations play out, you can explore some common business closure scenarios that entrepreneurs face.

Navigating Regional Variations Across the EU

While the broad ideas of bankruptcy and liquidation hold true everywhere, how they play out on the ground can be wildly different from one EU country to another. An entrepreneur thinking the process in Germany is a carbon copy of the one in Spain is setting themselves up for a nasty surprise. Every member state has its own legal traditions, its own jargon, and its own procedural quirks that can completely change the game for a struggling business.

This isn't a single, unified system. What one country calls "bankruptcy," another might label "insolvency proceedings" or "judicial liquidation," and those aren't just semantic differences—they come with entirely different rulebooks. The degree of court supervision, the authority given to a liquidator, and the pecking order of creditors are all dictated by national law.

Why Local Expertise Is Non-Negotiable

Trying to navigate this with generic, one-size-fits-all advice is a recipe for disaster. It can easily lead to non-compliance, unforeseen personal liability, and a process that drags on for far longer and costs much more than it should. For companies with operations, assets, or staff in multiple countries, the complexity skyrockets as you're suddenly juggling several legal systems at once.

For instance, the very definition of insolvency can vary. The priority given to different creditors' claims and the availability of restructuring options can also be worlds apart. One legal system might have robust frameworks designed to rescue a company, while another might push any business that falters straight into liquidation.

The key takeaway for any founder in the EU is this: local legal knowledge isn't a 'nice-to-have'—it's essential. Going it alone without country-specific expertise is like trying to find your way through a new city using a map for a different one. You're going to get lost.

Data Shows Drastic Differences in Bankruptcy Trends

The unique economic and regulatory climates across the EU also lead to huge variations in business failure rates. Recent EU data throws these regional differences into sharp relief, showing just how much bankruptcy declarations can fluctuate from one quarter to the next.

Consider this: Cyprus saw a staggering 399.3% jump in bankruptcy declarations in a single quarter, while Bulgaria was next with a 24.5% rise. Meanwhile, Poland was heading in the opposite direction, with declarations dropping by -17.3%. These numbers aren't just abstract statistics; they paint a clear picture of how local economies and legal frameworks shape the reality of business insolvency. You can dig into more of these findings on the European business statistics page on the Eurostat website.

These dramatic swings drive home a critical point for any entrepreneur. Your exit strategy can't be based on a general European concept; it must be built around the specific legal and economic realities of the country you operate in. The distinction between bankruptcy and liquidation is a practical one, defined by national laws that make localised guidance absolutely crucial for closing down properly.

Searching for a Faster Way Out? Exploring Alternatives

When you're dealing with a failing business, the last thing you want is a long, drawn-out process to close it down. Traditional bankruptcy and liquidation can feel like a labyrinth of paperwork and legal hoops, trapping founders in a state of limbo. For any entrepreneur, the thought of spending months—or even years—navigating this is a huge mental and financial drain. It stalls your ability to move on to the next venture and keeps the stress of a failed project hanging over your head.

Thankfully, there are now modern solutions designed to cut through this red tape. One of the most effective is a strategy called Liquidation Via Sale. It's a method built for one purpose: to give you a clean, swift, and final exit, bypassing the sluggish pace of conventional insolvency.

How Liquidation Via Sale Works

The concept is surprisingly simple but incredibly effective. Instead of you, the founder, having to manage the entire liquidation process yourself, you sell your company's shares to a specialist firm for a nominal amount. In one simple transaction, ownership is legally transferred, and so are all your responsibilities as a director.

From that moment on, the specialist firm takes over. They become the new owner and assume the full duty of winding down the company correctly. This means they handle all the legal filings, deal with creditors, and make sure everything is done by the book. For you, the original founder, it means you are immediately and legally out of the picture.

This approach completely flips the script. You go from being the person managing a slow, painful closure to being the client of a fast, efficient service. The personal weight is lifted almost overnight, freeing you up to focus your energy on what's next.

The Key Benefits for Founders

This kind of streamlined exit offers some very real advantages over sitting through a traditional process. The speed and sheer relief it provides are where the real value lies, and for many founders, that’s priceless.

Here’s what makes it so appealing:

Unmatched Speed: The entire ownership transfer can be done and dusted in just a few days. Compare that to the 6 to 24+ months you might be looking at for a standard liquidation or bankruptcy. If you want a better grasp of the timelines, our article on how long liquidation usually takes breaks it down.

Immediate Burden Removal: As soon as the sale is signed, you are no longer the director. That means an instant end to the administrative headaches, legal duties, and the emotional toll of running a company that's shutting down.

End to Creditor Communications: Dealing with constant calls and emails from creditors is one of the most draining parts of closing a business. Once the company is sold, the new owners handle all of that communication, giving you a clean break.

By offering a legal and efficient shortcut, Liquidation Via Sale bridges the gap between the overwhelming problem of a failed company and a practical, rapid solution. It allows you to legally and responsibly close one door so you can confidently open the next.

Common Questions from EU Founders

Closing a business chapter naturally brings up a lot of practical, often stressful, questions. Let's tackle some of the most common concerns EU founders have when they're trying to figure out the right path between bankruptcy and liquidation.

Can a Company Actually Recover After Bankruptcy in the EU?

Yes, it’s possible, but it’s a tough road and depends entirely on your country’s specific laws and the type of bankruptcy you enter. Many EU nations have reorganisation procedures, which work a bit like the Chapter 11 process in the US. The idea is to give a fundamentally sound business a bit of breathing room from creditors while it sorts out a repayment plan to get back on its feet.

Don’t mistake this for an easy out, though. This kind of restructuring is complicated, expensive, and offers no guarantee of success. It's a world away from liquidation, which is always a final act designed to shut the company down for good. Reorganisation is a battle for the company's life; liquidation is admitting the fight is over.

The chance to recover is probably the biggest single difference between bankruptcy and liquidation. Bankruptcy can be a lifeline for a business with a good core idea but bad finances. Liquidation offers no such second chance—it’s a definitive end.

Does Liquidation Always Mean the Business Failed?

Not at all. This is a huge misconception that trips a lot of people up. Sure, a compulsory liquidation is what happens when creditors force an insolvent company to close. But a Members' Voluntary Liquidation (MVL) is a deliberate, strategic move made by the owners of a company that is very much solvent.

Why would a successful business liquidate? Founders choose an MVL for plenty of good reasons:

They're ready to retire and want to exit gracefully.

A specific, successful project has reached its natural conclusion.

It's the most tax-efficient way to distribute the company's accumulated profits and assets among the shareholders.

Thinking of liquidation only as a sign of failure means you're only seeing half the story. A voluntary liquidation can be the final, planned chapter in a successful company's journey—a controlled exit, not a crisis.

As a Founder, What Happens to My Personal Assets?

This really comes down to your company's legal structure and the specific laws in your jurisdiction. If you've set up a limited liability company, your personal assets are generally shielded from the business's debts. That's the whole point of "limited liability."

But that shield isn't indestructible. There are a few scenarios where your personal wealth could be at risk:

If you've signed personal guarantees for any business loans.

If you're found guilty of fraudulent trading or other director misconduct.

If you haven't kept a clean line between your personal and company finances.

Be aware that both bankruptcy trustees and liquidators have a legal duty to dig into the directors' actions in the lead-up to the company's collapse. They will look closely at transactions and decisions to see if anything makes you personally liable. It's vital to get your head around these risks before you start either process.