Feb 12, 2026

Difference Between Dissolution and Liquidation: A Practical Guide for Founders

The core difference between dissolution and liquidation comes down to one simple idea: dissolution is the formal decision to close your company, while liquidation is the hands-on process of actually winding everything down.

Think of it like this: dissolution is firing the starting gun on the closure, not crossing the finish line.

Understanding the Initial Steps to Company Closure

When it’s time to close up shop, many founders get tangled in the legal jargon. This isn't just a matter of semantics; confusing these terms can lead to serious personal liability and a mountain of administrative headaches.

The first, most critical step is to grasp that dissolution is a decision, and liquidation is the action that follows. They are two distinct stages of the same journey: shutting down the business for good.

Dissolution is the official signal that you intend to cease trading. It's usually triggered by a shareholders' resolution, which effectively puts a stop to normal business activities. Crucially, though, it doesn't just wipe the company's obligations off the books.

Once that decision is made, the company enters a sort of legal limbo where its only purpose is to wind down. This is precisely where liquidation kicks in—a methodical process to settle every last corporate matter before the company officially ceases to exist.

Dissolution vs Liquidation at a Glance

To make this crystal clear, let's put the two concepts side-by-side. While they are intrinsically linked, their purpose, timing, and legal weight are worlds apart. One simply cannot happen without the other if the company has any financial footprint left.

Aspect | Dissolution (The Decision) | Liquidation (The Process) |

|---|---|---|

Primary Nature | A formal, legal declaration by shareholders to cease the company's operations. | The practical, administrative process of winding up all company affairs. |

Key Action | Filing official documents to signal the intent to close the company. | Selling assets, paying off creditors, and distributing any remaining funds. |

Timing | The first step in the company closure journey. It initiates the winding-up period. | The second, necessary step that follows the decision to dissolve. It finalises the closure. |

Legal Status | The company is officially 'in dissolution' but still legally exists to settle its affairs. | The company is actively being managed by a liquidator to finalise all obligations. |

Final Outcome | Marks the beginning of the end, but does not itself provide a clean closure. | Leads to the company being formally struck off the commercial register. |

This table shows how one is a legal starting point and the other is the practical execution. A clean exit requires both.

The most critical takeaway for founders is this: A company can be dissolved without being fully liquidated, leaving directors personally exposed to unresolved debts and legal challenges. This limbo state is a common and dangerous pitfall.

Global Context and Procedural Nuances

The line between these two stages can look different depending on where you are in the world. In some jurisdictions, for example, a company’s operational life ends with a shareholders' resolution for dissolution, but this simply kicks off the liquidation phase.

It's a serious issue. One study found a high number of company dissolutions, yet only a fraction actually proceeded to a full liquidation within the same year. This creates so-called 'zombie companies' that haunt the economy and their former directors.

Worse still, a dissolution process that stalls before liquidation can drag on for months or even years, a period during which directors remain personally liable for any outstanding debts. You can learn more about the wider economic impact from this detailed report on corporate dissolution.

Comparing the Legal and Financial Consequences

It’s one thing to know the dictionary definitions, but understanding the real-world legal and financial fallout is where the rubber truly meets the road. The path you choose—dissolution versus a full liquidation—directly impacts everyone from directors and shareholders to the creditors waiting for their invoices to be paid. This isn’t just about paperwork; it's about your personal financial security versus a future of undefined, lingering risk.

The biggest divide comes down to liability. Simply filing for dissolution doesn't make a company's debts or a director's legal duties vanish into thin air. It just signals you intend to close, leaving the door wide open for future claims if the winding-up process isn't formally and completely finished.

Director Liability: A Tale of Two Endings

For any company director, the most critical difference between these two paths is the finality of their personal liability. An incomplete closure—where a company is dissolved but never fully liquidated—creates a dangerous legal limbo.

In that scenario, directors stay personally on the hook. Creditors can, and often do, petition the court to have the company restored to the register just so they can sue it for outstanding debts. This means you could be facing legal action for the company's unpaid bills months, or even years, after you thought the business was a closed chapter.

Formal liquidation, however, is designed to draw a clear, legally-binding line in the sand. An appointed liquidator takes control of the entire process, settles all debts, and finalises the company's affairs. Once this is done and the company is struck from the commercial register, the directors' duties and personal liabilities are officially extinguished. It provides a clean break. This isn't just a theoretical difference; it's a harsh lesson many founders learn the hard way. For a deeper look at this, you might find our guide on the differences between bankruptcy and liquidation for EU founders useful, as it explores these liability issues further.

How Creditors Are Treated

How your creditors are handled is another major point of contrast. The approach you take directly affects their chances of getting paid and shapes the legal risk you and your fellow directors carry.

Under Dissolution: If a company is just dissolved without a proper liquidation, there's no organised system for paying creditors. This informal approach often means creditors get left out in the cold, legally empowering them to come after the directors personally for the company's debts. It’s a reactive and incredibly risky method.

Under Liquidation: This is a structured, legally-mandated process. A licensed liquidator identifies all company assets, sells them, and pays out the proceeds to creditors according to a strict legal order of priority. It doesn't guarantee every creditor gets paid in full, but it ensures the process is managed fairly, transparently, and by the book.

A critical point to remember: you cannot legally dissolve a company that still has outstanding debts without going through liquidation. Trying to do so is a serious breach of your director's duties and can lead to severe penalties, including disqualification.

Final Tax and Accounting Obligations

The final financial wrap-up also looks very different, highlighting just how thorough a proper liquidation is compared to a standalone dissolution.

Simply filing for dissolution doesn't settle your accounts with the tax authorities. The company is still required to prepare and submit final accounts and tax returns covering the period right up to when it stopped trading. If you don't, you can rack up fines and penalties that will follow you.

Liquidation formalises this entire process. The liquidator is responsible for preparing the final statement of accounts, dealing with the tax authorities to settle any outstanding liabilities, and getting all the necessary clearances. This ensures every financial loose end is neatly tied up, preventing future tax headaches.

To bring this home, an insolvency study found a 25% rise in personal bankruptcy filings directly linked to directors of companies left in a 'dissolved but not liquidated' state. The same report showed that a staggering 41% of directors from these firms faced disqualifications, compared to just 12% in formal liquidations. This data powerfully illustrates the protective shield a properly managed liquidation provides.

The following table breaks down these crucial differences point-by-point.

Detailed Comparison of Legal and Financial Effects

Criteria | Dissolution | Liquidation |

|---|---|---|

Director Liability | Remains ongoing and indefinite. Creditors can pursue directors personally if debts are unpaid. | Formally extinguished once the process is complete and the company is struck off the register. |

Creditor Rights | Unprotected. Creditors must take legal action, often against directors, to recover debts from a dissolved company. | Protected and structured. An independent liquidator ensures assets are distributed fairly according to legal priority. |

Legal Finality | Incomplete. The company can be restored to the register by creditors or authorities to pursue claims. | Definitive. Provides a legally conclusive end to the company's existence and its directors' duties. |

Tax Obligations | Director's responsibility. Directors must file final accounts and returns. Failure results in personal penalties. | Liquidator's responsibility. The liquidator handles all final tax filings and obtains clearance from authorities. |

Asset Distribution | Unregulated. Directors distribute remaining assets, risking improper preference claims if creditors are unpaid. | Regulated and transparent. Assets are sold and distributed by a licensed professional following strict legal rules. |

Public Record | The company is marked as "dissolved," which can be a red flag for future ventures or credit checks if debts were left. | The company is marked as "liquidated," a formal and recognised end-of-life process. |

At the end of the day, the fundamental difference between dissolution and liquidation is about finality. Dissolution alone is an unfinished story, leaving directors and the company itself in a vulnerable, unresolved state. Liquidation is the final chapter, ensuring every legal and financial duty is met and offering the only true path to a clean and conclusive exit.

Timelines, Steps, and Costs: The Reality on the Ground

It's one thing to grasp the legal difference between dissolution and liquidation, but it’s another thing entirely to live through the practicalities of each. The procedures, timelines, and costs are worlds apart, and for founders, this is where the theory hits the hard reality of bureaucracy and financial strain.

The paths diverge right from the very beginning. Kicking off a dissolution often feels straightforward—a simple shareholder resolution and some initial paperwork filed with the relevant company register. This first step is deceptively easy, but it really just starts the clock on what can become a much longer, more complicated affair.

Liquidation, on the other hand, is a serious undertaking from day one. It demands the formal appointment of a licensed liquidator, a third-party professional who takes legal control of the company to wind it up properly and by the book.

The Procedural Roadmap for Closing Your Company

While the exact requirements shift depending on the jurisdiction, the general flow for each process is pretty distinct. The dissolution path might look shorter on paper, but it often leaves the company in a vulnerable, unfinished state. Liquidation is the comprehensive, end-to-end procedure designed for true finality.

Typical Steps in Dissolution (as an initial stage):

Shareholder Resolution: The owners formally vote to stop all business activities and start the winding-up process.

Initial Filings: Directors submit the required forms to the commercial register, officially signalling their intent to dissolve.

Public Notice: The plan to dissolve is usually published in an official gazette, giving creditors and other interested parties a window to object.

This is often where the 'simple' part ends. If your company still has any assets or liabilities, it cannot legally be struck off the register. To finish the job, you have to move on to the next stage: liquidation.

Typical Steps in Formal Liquidation:

Appoint a Liquidator: A licensed insolvency practitioner is brought in to take charge and oversee the entire process from start to finish.

Realise the Assets: The liquidator takes control of everything the company owns—from cash in the bank to equipment and stock—and sells it all off.

Settle with Creditors: All known creditors are contacted and their claims are verified. The money raised from selling the assets is then used to pay off company debts according to a strict legal pecking order.

Final Reporting and De-registration: Once the debts are settled, the liquidator prepares final accounts, squares away any remaining tax obligations, and files a final report. Only then can the company be formally and permanently removed from the register.

Unpacking the True Cost in Time and Money

For most founders, the biggest shock comes down to time and money. A traditional company closure is neither quick nor cheap. The timelines can be punishingly long, often stretching from many months into several years, all while legal and administrative costs keep piling up.

A common mistake is underestimating the hidden costs. It's not just about the official filing fees; you must account for legal advice, notary services, and the liquidator's professional fees, which can easily run into thousands of dollars.

This drawn-out timeline is a huge source of stress and ongoing risk. Historical data from one country, for example, shows the full dissolution-to-liquidation cycle took a gruelling 22 months on average, with 45% of cases getting stuck in notary-related delays. Even after digital reforms, streamlined liquidations still took 13 months. These hold-ups have real consequences: the lengthy process led to thousands of 'dormant entity' penalties, hitting directors with substantial fines. You can see more on these procedural challenges in this EY report.

The financial hit is just as serious. Legal and advisory fees for a standard liquidation can range from a few thousand to tens of thousands of dollars, depending on how complex the company's affairs are. For a startup that has already burned through its cash, these costs can be impossible to meet. You can get a better sense of what to expect by reading our detailed guide on how long company liquidation typically takes. This stark reality forces founders to face the true investment needed for a clean legal exit, highlighting the massive gap between filing a simple dissolution notice and completing a professionally managed liquidation.

Real-World Scenarios: Choosing the Right Path

Knowing the textbook definitions of dissolution and liquidation is one thing, but applying that knowledge in the real world is what keeps you out of legal hot water. The choice you make isn't just a matter of paperwork; it’s a direct reflection of your company's financial state at the finish line, and it determines how cleanly you can walk away. Get it wrong, and a simple wind-down can spiral into a multi-year headache.

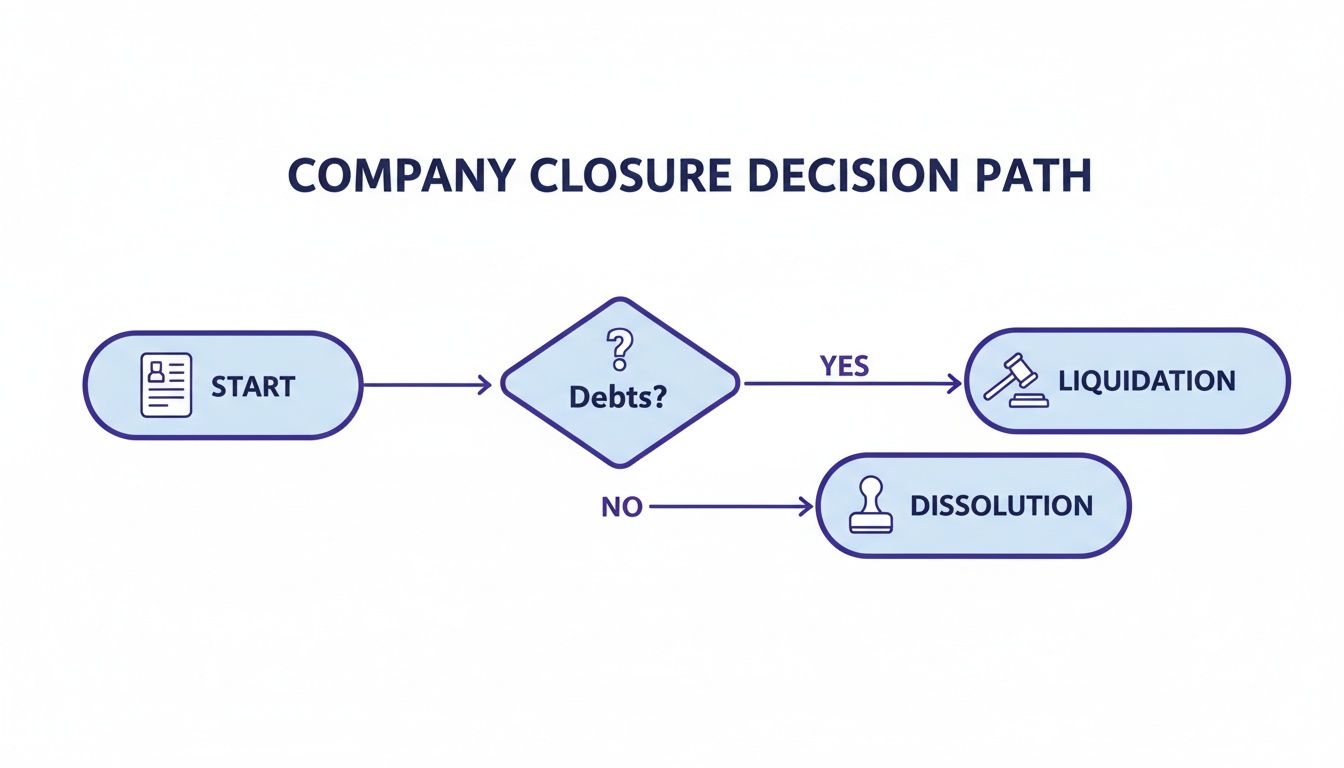

Ultimately, the decision hinges on one critical question: does the company have any outstanding debts or unresolved business? This simple flowchart gets right to the heart of the matter.

As you can see, the moment liabilities enter the picture, you're on the path to a formal, structured liquidation. It's the definitive fork in the road.

When Simple Dissolution Makes Sense

A straightforward dissolution, or "strike-off," is really only an option for a very specific, and frankly, rare, type of company. This route is reserved for businesses that are completely "clean." That means they've stopped trading, have no assets left, and—most crucially—owe absolutely nothing to anyone.

Here are a couple of classic scenarios where dissolution is the right move:

The Dormant Shell Company: A founder registers a company for a great idea that just never got off the ground. The company never traded, never had a bank account, and has no creditors. Dissolution here is just a simple, cheap administrative task to get the dormant entity off the official register.

The Retired Solopreneur: Think of a consultant who ran their business through a limited company and is now ready to retire. They've meticulously paid every supplier, settled their final tax bill, and cleared out the company bank account. With a zero balance and no loose ends, dissolution is the perfect final step.

It cannot be stressed enough: even a tiny, forgotten supplier invoice or a small outstanding tax liability legally bars a company from using simple dissolution. Trying to strike off a company with debts is a serious breach of your duties as a director and can expose you to personal liability.

When Formal Liquidation is Unavoidable

For the vast majority of companies winding down, even those that seem straightforward, a formal liquidation is the only legally compliant and responsible way to close. This process is specifically designed to manage complexity and give directors a legally binding finality, protecting them from future problems.

Liquidation isn't just for failing businesses; it becomes a necessity in any of these common situations:

Companies with Any Creditors: This is the number one reason. If your business owes money—to suppliers, a landlord, the tax authorities, or a bank—you are legally obligated to enter liquidation. A liquidator's job is to ensure assets are sold and distributed fairly among these creditors, all by the book.

Significant Assets to Distribute: Let's say a company stops trading but still has valuable assets on its books, like cash in the bank, property, or valuable intellectual property. It must be liquidated. This creates a transparent and legally robust process for selling those assets and distributing the cash to shareholders once all debts are settled.

Shareholder or Director Disputes: When business partners can't agree on how to wind things down, appointing an independent, third-party liquidator is the only way forward. The liquidator acts as a neutral referee, managing the closure impartially and stopping disagreements from turning into expensive court battles.

Insolvency: If a company's liabilities outweigh its assets, it's insolvent. In this case, liquidation is inevitable. Creditors can force a compulsory liquidation, but directors can often opt for a Creditors' Voluntary Liquidation (CVL). This allows them to retain a degree of control and show they are acting responsibly.

Choosing the right path comes down to legal compliance and personal risk management. The low cost and simplicity of dissolution can be tempting, but it’s a safe option only for the very cleanest of company closures. For any business with a financial footprint, no matter how small, formal liquidation is the only route to a truly clean break.

The Dangers of an Incomplete Company Closure

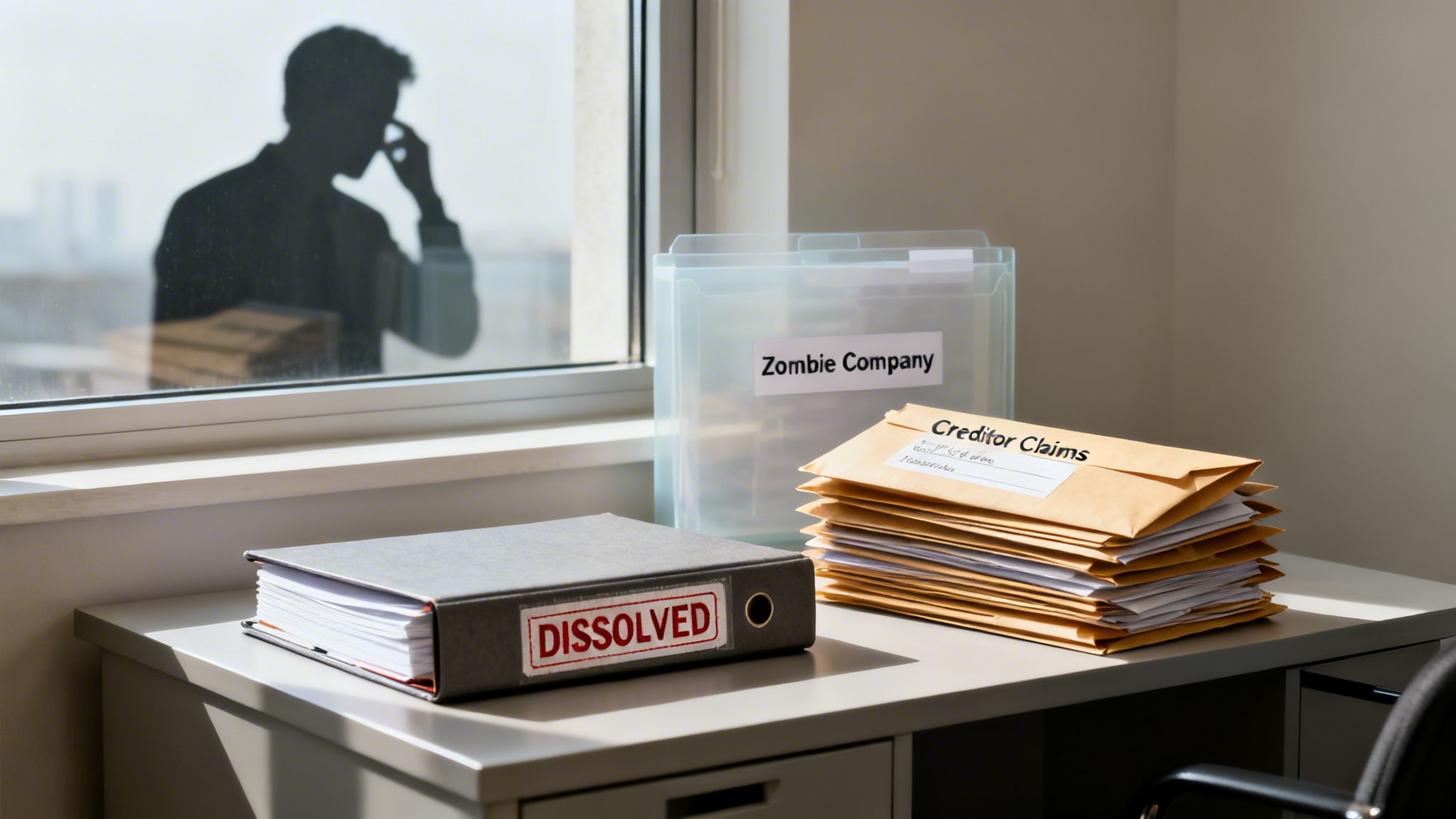

Getting the distinction between dissolution and liquidation right isn't just a matter of semantics—it's about managing massive personal risk. If you mishandle your company's final chapter, you can turn what should be a clean exit into a legal and financial nightmare that follows you for years. The biggest and most common mistake? Creating a 'zombie company'.

A zombie company is one that’s been struck off the register—dissolved on paper—but never properly wound up. It's stopped trading, but its debts and legal obligations are still hanging around, waiting to cause trouble. For a director, this limbo state is incredibly dangerous.

Personal Liability: The Ghost That Lingers

Here's the critical danger: personal liability. Too many directors believe that simply filing for dissolution shields them from the company's debts. That's a very expensive mistake to make.

If you dissolve a company that still owes money—to suppliers, tax authorities, or even a landlord—those creditors don't just give up. They can apply to the court to have the company restored to the register. The business is essentially brought back from the dead for one reason: so they can sue it for the money they're owed.

When this happens, the spotlight quickly moves from the revived company to the directors. Not following the proper winding-up process is a breach of your duties, and the courts can make you personally liable for the company's outstanding debts. Suddenly, your home, savings, and other personal assets are on the line. To get a clearer picture of these risks, it’s worth understanding how director liability for company debts really works.

An incomplete closure doesn't make debts disappear; it merely transfers the risk from the company to you. A full liquidation is the only process that formally and legally extinguishes these liabilities.

The Red Flags of a Failing Closure

You need to know when a company closure is going wrong, and fast. An incomplete shutdown rarely happens overnight; it’s usually a slow slide caused by cutting corners or missing crucial steps.

Keep an eye out for these warning signs that you're creating a zombie company:

Lingering Creditor Claims: This is the most glaring red flag. If you’re getting invoices, payment demands, or legal letters for old company debts after you've filed for dissolution, you have a problem.

Ignoring Official Correspondence: Letters from tax agencies, company registries, or other regulators can’t be ignored. Failing to respond leads to automatic penalties and can trigger an investigation.

Unresolved Bank Accounts: Leaving a company bank account open, even with a tiny balance, can block a clean strike-off and attract scrutiny.

Failing to File Final Accounts: Even a dissolved company needs final tax returns and accounts. Ignoring this duty means fines will start piling up, which can eventually become your personal responsibility.

These aren't just minor admin issues; they point to a fundamentally broken closure process that leaves you exposed. The consequences can be serious, ranging from substantial fines to being disqualified as a director for years. In the worst-case scenario, it can lead to personal bankruptcy, wrecking your finances and your ability to start another business.

Your Top Questions About Closing a Company

When you're at the end of a company's journey, a lot of questions pop up, and they're usually urgent. Getting the difference between dissolution and liquidation straight is fundamental to making smart choices that shield you from personal risk. Here, I'll tackle the most common queries I hear from founders, cutting through the jargon to give you practical answers for a clean exit.

Many of these questions come from a place of real concern, and for good reason. Choosing the wrong path—or worse, not finishing the process at all—can have serious legal and financial blowback.

Can I Just Dissolve My Company and Walk Away if It Has Debts?

Absolutely not. This is probably the single most dangerous misunderstanding I see when it comes to closing a business. Dissolution is just the first step—it's like announcing you plan to close. If your company owes money or still owns assets, you are legally required to go through a full liquidation to formally wind things up.

If you just file for dissolution and hope for the best, you're leaving yourself wide open. Directors can be held personally liable for the company's debts. Creditors have every right to come after you personally, which could lead to everything from personal bankruptcy and fines to being disqualified as a director. A formal, complete liquidation is the only way to draw a legal line in the sand and protect your personal finances.

How Long Does a Traditional Liquidation Process Take?

There's no single answer as it depends on where you are, but one thing is certain: a traditional liquidation is never fast. Realistically, you should be prepared for the process to take anywhere from 6 to 24 months. And that's if things go smoothly. If you run into creditor disputes, have complex assets to sell, or get tied up in tax audits, it can drag on for even longer.

This isn't just about waiting. That whole time, the stress continues, the paperwork keeps piling up, and as a director, you're still on the hook. You're not truly free from your legal duties until the company is officially struck off the commercial register.

The sheer length and unpredictability of traditional liquidation is a huge source of pain for founders. During those long months, directors are stuck in limbo, unable to fully move on to their next project while they wait for an external liquidator to slowly untangle the company's affairs.

What Happens if I Don’t Formally Liquidate a Dissolved Company?

Failing to properly liquidate a company that still has debts or assets creates what's often called a 'zombie company'. It might be gone from the active register, but legally, it's in a state of suspended animation—and so are your responsibilities as a director.

This is where things can get really messy. You remain legally accountable for its debts and any missed filings. This can trigger a whole host of problems:

Mounting Fines: Penalties for unfiled accounts and tax returns don't just stop; they keep adding up.

Personal Liability: Creditors can go to court to have the company reinstated, which then allows them to take legal action directly against you.

Director Disqualification: Regulators can ban you from being a director for years.

The only way to avoid this and achieve a clean, legal end is to see the liquidation process through to its formal conclusion. That's what officially extinguishes the company and your duties along with it.

What Is the Main Difference in the Final Outcome for Directors?

This is the bottom line, the most critical distinction, and the reason you need to get this right. The path you choose determines whether you get a genuine fresh start or stay tangled in old liabilities for years to come.

An incomplete closure—just dissolving the company—leaves it in a dangerous legal grey area. As a director, your liabilities don't disappear, and there’s always a risk the company could be brought back from the dead to face legal claims. Your exposure has no end date.

In contrast, a full and proper liquidation results in the company being formally and permanently removed from the commercial register. It provides a definite, legally recognised end. Corporate debts are wiped out (as long as you haven't personally guaranteed them), and directors are officially released from their duties and the personal liabilities that come with them. It’s the only way to truly close one chapter and confidently start the next.