Feb 23, 2026

How to Close Dormant Company: The Founder's Exit Guide

First things first, let's get one thing straight: knowing how to close a dormant company means understanding it's a formal legal process. You can't just walk away and hope for the best. Properly dissolving the company involves settling its affairs and filing specific paperwork with the authorities. This is the only way to officially end its existence and protect yourself from any future trouble.

Why Your Dormant Company Is a Hidden Liability

That company you registered with big dreams, the one that never quite launched? It might seem harmless collecting dust in the background. After all, if it's not trading, it can't cause any problems, right?

Unfortunately, that's a common and expensive misunderstanding. A dormant company isn't just inactive; it's a ticking clock of hidden costs and legal risks that can bite you when you least expect it.

Even without a single sale, your company is still a legal entity with very real obligations. It quietly accumulates administrative chores and potential penalties if you don't keep up. Think of it like a car you no longer drive but is still registered in your name—you're on the hook for its tax and insurance, and you're liable if something goes wrong.

The Slow Bleed of Costs and Compliance

The most immediate threat from a dormant company is the slow, steady drain on your bank account. It’s not making you any money, but it’s certainly costing you. These expenses are easy to overlook until they snowball into a genuine problem.

Here’s what those hidden liabilities usually look like:

Annual Filing Fees: Most jurisdictions demand an annual report or confirmation statement, even for companies that aren’t trading. Miss the deadline, and you’ll start racking up fines that grow over time.

Registered Agent and Office Fees: Your company legally needs a registered address, and often a registered agent. These services have annual renewal costs that don't just vanish because your business is on pause.

Accountancy Costs: Even filing "nil" or dormant accounts often requires an accountant to prepare everything correctly. That’s another professional fee added to the pile.

Bank Account Fees: Many business bank accounts come with monthly service charges. These can easily add up to hundreds a year for an entity that's doing absolutely nothing.

I see this all the time with non-resident founders of international companies. They set up a business, but the venture stalls. A year or two later, they’re hit with official letters demanding payment for missed filings and accumulated penalties. A forgotten side project suddenly becomes a very real financial headache.

The Legal Risks of Inaction

Beyond the mounting costs, simply ignoring a dormant company exposes you to serious legal risks. From a regulator's point of view, there isn't much difference between an inactive company and a non-compliant one. As a director, you are still legally responsible for the company's affairs.

Forgetting about these duties can have some pretty severe consequences. For instance, repeatedly failing to file the required documents can lead to the company being "struck off" the register against your will. While that might sound like a convenient, free way to close down, it can actually leave you personally liable for any of the company's remaining debts. It can also tarnish your professional reputation, making it much harder to get funding or a director role in the future.

Closing your company properly isn't just a bit of admin. It's a crucial step to protect your finances, steer clear of legal trouble, and free yourself up to focus on your next venture without old baggage holding you back.

Choosing Your Exit: Traditional Dissolution vs. Accelerated Sale

So, you’ve realised that dormant company isn't just sitting there quietly—it's a genuine liability. The next logical step is figuring out how to shut it down for good. You've essentially got two roads you can take, and they lead to very different places in terms of time, cost, and how much work you’ll have to do yourself.

The first option is what we call traditional dissolution. This is the classic, by-the-book procedure for formally closing a company. It’s a methodical, often slow-moving process that ensures every legal and financial loose end is neatly tied up before your company is struck from the official register.

The second, much faster route is an accelerated sale. Here, you transfer ownership of your company to a specialised firm. They take on the legal burden of winding it down properly, letting you walk away with a clean break.

Understanding Traditional Dissolution

Think of traditional dissolution as a bureaucratic marathon. It demands patience and a lot of admin. While the exact steps differ slightly across countries, the fundamental stages are pretty much the same everywhere—they're designed to be thorough.

Typically, you'll have to go through:

A Shareholder Resolution: The decision to close up shop has to be formally documented, usually through a shareholder vote or a written agreement.

Appointing a Liquidator: This person takes control of the company to sell off any assets, pay any debts, and distribute what’s left to the shareholders.

Notifying Authorities and Creditors: You’ll need to make public announcements to inform tax agencies, government bodies, and potential creditors that the company is closing. This gives them a chance to file any claims.

Final Filings and Tax Clearance: The liquidator prepares the final accounts and tax returns. Only once the tax office gives the all-clear can the company finally be struck off the register.

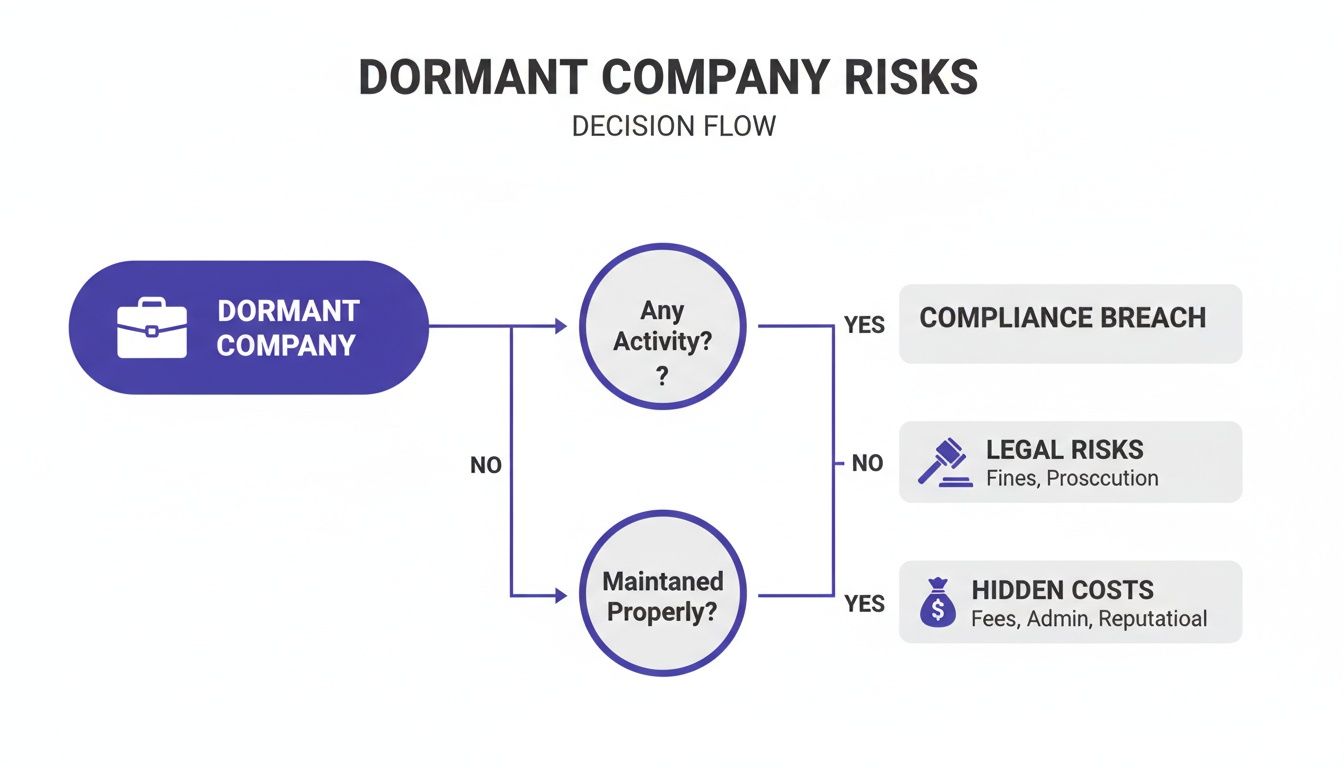

This path is all about ticking boxes, but as you can see below, leaving those boxes unticked creates some serious headaches.

As the visual shows, a dormant company can quickly become a minefield of hidden costs and legal risks. That's why having a clean, decisive closure plan is so important.

The Alternative: An Accelerated Sale

If traditional dissolution is a marathon, an accelerated sale—also known as a Liquidation Via Sale—is a sprint. It's built for founders who just want to move on, quickly and definitively. Instead of slogging through the dissolution process yourself, you effectively sell the problem to someone else.

Here’s a practical look at how it works: you sign an agreement with a specialist firm, like EndCorp, to sell all the shares in your company for a nominal amount. The moment that sale is complete, they become the new legal owners.

Your involvement essentially ends the day the share transfer is signed. The new owner assumes all director responsibilities and handles the entire winding-down process, including dealing with creditors and filing final paperwork. You walk away clean.

This approach is a lifesaver for founders who don’t live in the country where their company is registered or for e-commerce sellers with complicated business structures. The headache of navigating a foreign bureaucracy is completely removed. While there are technical differences between dissolution and liquidation, this hybrid sale model bypasses the typical complexities of both. You can learn more about this in our guide on the difference between dissolution and liquidation.

Which Path Is Right for You?

Choosing between these two options really boils down to your priorities. To help you decide, here's a quick side-by-side comparison of how each method stacks up.

Traditional Dissolution vs Liquidation Via Sale at a Glance

Factor | Traditional Dissolution | Liquidation Via Sale |

|---|---|---|

Timeline | 6-24 months (or longer) | 3-30 days |

Cost | High (legal, accounting, liquidator fees) | Fixed, predictable fee |

Founder Involvement | High (ongoing paperwork, communication) | Low (only during the initial sale) |

Liability | Founder remains responsible until the very end | Transferred to the new owner on day one |

Ultimately, traditional dissolution gives you a sense of direct control, but you pay for it with your time and often with high professional fees. You're on the hook until the entire, lengthy process is over.

An accelerated sale, on the other hand, gives you speed and certainty. It’s the ideal choice for founders who need to close one chapter and get on with the next, without an old company holding them back.

Deciding to close your dormant company the old-fashioned way? Be prepared for what often feels like a bureaucratic marathon. While this route is designed to be meticulous, ensuring every single legal and financial thread is neatly tied, it demands a huge amount of your time and patience.

This isn't a quick sale; it's a slow, formal wind-down. You’ll be navigating a series of compulsory steps that can stretch out for months—or in some cases, even years. All the while, you’re still legally on the hook for the company. The goal is to formally dissolve the business, but the path is often littered with administrative hurdles.

Kicking Off the Closure with a Shareholder Meeting

The first real step is getting all the owners to officially agree on the closure. This is more than a quick chat; it’s a legal necessity. You have to hold a formal shareholder meeting to pass a resolution to wind up the company and kick-start the liquidation process.

This resolution isn’t just a handshake deal. It needs to be officially recorded in the meeting minutes and then filed with the appropriate company registry. For founders who don't live in the country, or for partnerships with stakeholders spread across the globe, just getting everyone together for this meeting can be a logistical nightmare, adding immediate delays.

Once the resolution is passed, you’ll need to appoint a liquidator. This is a critical step. This person or firm officially takes the reins of the company and manages the entire shutdown from here on out.

A liquidator's job is a big one. They're tasked with tracking down and selling any remaining assets, formally notifying creditors, and settling every last financial obligation before the company can be legally put to rest. You're handing over the keys, but you're not quite off the hook yet.

The Public Announcement and Creditor Period

With a liquidator appointed, the process goes public. You're legally required to publish an announcement in an official gazette or a national newspaper, declaring your plan to close the company. This isn't just for show—it's a public notice for any potential creditors.

This announcement starts a mandatory waiting period, which usually lasts for several months. During this window, anyone who thinks the company owes them money can come forward and make a claim. It’s the liquidator’s job to verify and settle these claims.

Here’s a taste of what that involves:

Notifying Tax Authorities: The local tax office must be formally notified. They will then run their own audit to make sure all your tax returns are filed and every penny of tax has been paid.

Informing Other Government Bodies: Don't forget social security agencies and any other relevant government departments. They need to be told, too.

Dealing with Commercial Creditors: Any suppliers, landlords, or other business partners with unpaid invoices will need to be settled using whatever company assets are left.

This stage can move at a glacial pace. In some notoriously complex countries, the red tape feels almost designed to be difficult. Take Indonesia, for example. A company has to be inactive for three years before it can even apply for dissolution. The process then involves a court petition that can take 6-12 months, public notices, approvals from multiple ministries, and a full tax clearance. Potential fines for past non-compliance can hit €6,000.

In 2022, only a mere 12,500 dormant companies in Indonesia were successfully closed this way, leaving countless founders stuck with ongoing liabilities and stress.

Final Hurdles and Unexpected Costs

Once the creditor period is over and all known debts are paid, the liquidator draws up the final accounts. These documents are the proof that all assets have been liquidated and all liabilities have been settled. But you're not done yet.

Only after the tax authorities have reviewed these final accounts and issued a clearance certificate can the company finally be struck off the register.

This is often where the nasty surprises pop up. If the tax audit digs up old compliance issues—like unfiled annual reports or unpaid taxes from when the business was still active—you’ll be hit with fines and back-payments. These can easily run into thousands of euros, turning a supposedly simple closure into a costly headache.

For founders who want to sidestep this long and winding road, understanding what striking off a company entails can offer a much-needed alternative perspective. This traditional journey, stretching anywhere from 6 to 24 months, is a perfect illustration of why so many founders are now looking for a faster, cleaner exit.

The Accelerated Exit: Your Step-by-Step Walkthrough

If the thought of traditional dissolution makes you wince at the months of paperwork and legal red tape, you're not alone. The good news is that there’s a much more efficient way forward, built for founders who value their time and need a definitive, clean break. It’s known as an accelerated exit, or more formally, a Liquidation Via Sale.

Instead of personally navigating the winding-down process, you simply sell the entire company to a specialist firm. They take complete ownership and handle every last detail of the closure, allowing you to walk away in days, not months. Let's look at exactly how this works from your point of view.

Initial Consultation and Contract Review

The whole thing kicks off with a straightforward, no-obligation chat. You'll briefly explain your company's situation—where it's registered, its current status, and if there are any outstanding liabilities. This initial check allows a service like EndCorp to confirm your company is a good candidate for this method.

Assuming it's a match, you'll receive a clear contract to review. This document spells out the entire process, the fixed fee, and the legal transfer of ownership. Transparency is absolutely crucial; you should understand every clause and be confident there are no hidden fees or surprises down the line.

This first phase is all about making sure everyone is on the same page. You get a complete picture of the cost and timeline before you commit to spending a single euro.

Signing the Share Transfer and Making Payment

Once you're comfortable with the terms, the key step is signing the share transfer agreement. This is the legal document that officially passes ownership of your dormant company from you to the specialist firm. For most founders, especially those living abroad, this is all handled remotely with secure digital signatures.

Right after signing, you'll make the one-time payment for the service. This fixed fee covers absolutely everything required to close the company, from start to finish. It’s a welcome contrast to the unpredictable, and often escalating, costs that can come with a traditional dissolution.

The moment the agreement is signed and your payment is confirmed, your legal responsibility as a director is over. This is the clean break you're after. The new owner immediately takes your place on the company register.

How Liabilities and Creditors Are Handled

A natural question for any founder is, "What happens to the company's debts?" When you opt for a Liquidation Via Sale, the liabilities are transferred right along with the company. The new owner—the specialist firm—legally assumes the duty to manage and settle any valid creditor claims according to local law.

This means you will stop receiving payment demands or calls from creditors. The firm takes over all that communication, shielding you from any further stress or involvement. It's a key part of the legal framework that makes this a secure and valid closure method in many jurisdictions.

The efficiency here can't be overstated. For example, in a jurisdiction like Indonesia, a traditional liquidation takes an average of 4–8 months and racks up legal fees of €3,000–€9,000. This is a huge burden, especially for the 65% of owners who are non-residents. An accelerated sale bypasses all of that. If you're curious, you can explore more insights about company statuses in Indonesia to see the challenges founders face.

Final Steps and Removal from the Registry

With the new owner officially in place, your part in this is done. You are free to move on to your next project, confident that your old company is being professionally and legally wound down.

Here’s a quick look at what the firm handles behind the scenes:

Updates the Company Registry: They immediately file the paperwork to have your name officially removed as a director and shareholder.

Manages Final Compliance: The firm takes care of all remaining administrative duties, like filing final accounts and tax returns, to formally dissolve the company.

Handles All Communication: Any future letters or emails from government agencies or creditors are directed to them.

This accelerated exit is designed for one thing: finality. It gives you a legal, fast, and stress-free way to untangle yourself from a dormant business, freeing up your mental energy and resources for what's next. For founders asking how to close a dormant company without the pain, this is the definitive answer.

Common Pitfalls and Red Flags When Closing a Company

I've seen it time and time again: a founder thinks closing a dormant company is just a matter of filing a form and walking away. In reality, it's more like navigating a minefield. One wrong step can lead to serious, long-term personal consequences. Understanding the red flags before you start is the key to a clean exit.

Let’s get into the most common mistakes I see founders make and the situations that can turn a simple closure into a legal and financial nightmare.

The Myth of “Just Let It Die”

One of the biggest, and most tempting, mistakes is to simply abandon the company. The logic seems sound, right? If you stop filing annual reports and paying fees, the government will eventually strike it off the register for you. Problem solved.

Except, it isn't. While this might eventually happen, it's not a proper closure; it’s a black mark for non-compliance. This passive approach leaves you wide open. Authorities can—and do—chase directors for unpaid fees and penalties that piled up before the strike-off. Even worse, if there were any old company debts, creditors could argue you acted negligently, potentially making you personally liable.

That Forgotten Personal Guarantee

This is the hidden trap that catches so many founders. Think back to when you were starting out. Did you sign a personal guarantee for a business loan, a property lease, or even a supplier account? It's incredibly common.

These agreements don't just vanish when the company goes dormant.

A personal guarantee is a legal tool that "pierces the corporate veil," connecting the company's debts directly to your personal finances. If you try to shut down without settling that specific debt, the creditor has a legal right to come after you and your personal assets—your house, your savings, everything.

You absolutely must dig through every contract you ever signed. Missing a personal guarantee can quickly turn a straightforward company closure into a personal financial catastrophe. If you find one, that debt has to be dealt with head-on before you even think about starting the closure process.

Active Criminal or Fraud Investigations

This should be a no-brainer, but it needs to be said. If your company is under any kind of criminal or fraud investigation, attempting to close it down is a terrible idea. It can be seen as a direct attempt to obstruct justice.

No legitimate dissolution can happen under these conditions. We’re talking about situations like:

Investigations into money laundering.

Allegations of fraudulent trading.

Serious inquiries from tax authorities about potential tax evasion.

Trying to close a company in this position will only make your legal problems much, much worse. The entire process must be put on hold until every investigation is completely finished. Be upfront with any legal advisors about these issues—they need to know.

Lingering Debts and E-commerce Messes

For anyone in e-commerce, platform-specific issues can be a real headache. Maybe your Amazon or Shopify account got banned, and now you're left with unresolved customer claims, trapped inventory, or unpaid platform fees. These are company liabilities, and they must be sorted out.

The same goes for any other unresolved debts, no matter how small. It’s tempting to ignore a few hundred quid here or there, especially in jurisdictions where authorities seem slow to act. For instance, in Portugal, a staggering 200,000 PT companies are sitting dormant. Of those, 35% have failed to meet tax compliance for three years straight.

But don't let those numbers fool you into a false sense of security. While formal dissolutions are low, official data from 2022 showed that 22% of dormant companies facing creditor pressure were hit with forced interventions, costing owners 2-5% of their personal assets in sanctions. You can find more detail on incorporated company trends via the UK government's publishing service.

Ignoring these debts won't make them disappear. Any creditor can object to your company's closure, which will stall the process indefinitely and rack up more costs. Before you start, it’s vital to understand the full scope of your director liability for company debts.

Knowing these pitfalls isn't meant to scare you. It’s the first step in learning how to close a dormant company the right way and deciding whether you have a simple case or a more complex situation that needs a different strategy.

Got Questions About Closing Your Dormant Company? We've Got Answers

Even when you've decided it's time to move on, closing a company can feel like a maze of unknowns. It's a big step, so it's natural to have questions. Here are the answers to the queries we hear most often from founders, giving you the clarity you need to shut down your dormant company for good.

What Happens to Company Debts in an Accelerated Sale?

This is usually the first thing people ask. When you use an accelerated service, the legal ownership of your company is transferred to a new owner. This transfer includes everything—all assets and, crucially, all liabilities.

From the moment the sale is finalised, the new owner takes on the full legal responsibility for handling any legitimate creditor claims, following all local regulations. Your personal liability is cut off, provided you haven't signed any personal guarantees for the company's debts. The entire process is structured to create a clean break, legally shielding you from future creditor contact.

Can I Close My International Company if I’m Not a Resident?

Yes, absolutely. In fact, this is where an accelerated exit really shines. For founders living abroad, trying to close a company the traditional way can be a bureaucratic nightmare. You're often dealing with local representatives, getting documents notarised, and trying to understand a system you're not familiar with—all from a distance.

Services like EndCorp are built specifically for non-resident owners. The whole thing, from signing the initial agreement to the final ownership transfer, is managed remotely. You won't need to worry about expensive flights or booking in-person appointments, making it a genuinely practical solution for entrepreneurs around the world.

What if My Company Has No Assets? Am I Still Eligible for a Service Like EndCorp?

Yes, you can still be eligible. Most dormant companies don't have any assets; many have a zero balance sheet or even carry some liabilities. That's the reality for many businesses, and a Liquidation Via Sale is designed to provide a legal and fast exit for exactly these kinds of non-viable or inactive companies.

Eligibility isn't really about assets. It's more about the company's legal status. The main requirements are usually straightforward:

The company can't be under any active criminal investigation.

You must be transparent about any personal guarantees you've signed.

The service can't be a tool to escape legitimate personal liabilities.

A quick, free chat is usually all it takes to see if your company qualifies for this type of swift exit.

How Much Will It Cost to Close My Dormant Company?

The cost can vary hugely depending on which method you choose. Going the traditional dissolution route is often surprisingly expensive and slow. You could easily be looking at costs anywhere from €3,000 to €10,000 or more, once you add up liquidator fees, legal filings, and the fines that can rack up over a 6 to 24 month process.

In contrast, an accelerated service like EndCorp works with a fixed fee, usually starting around €2,000. This gives you complete certainty on cost from the very beginning. It's often the cheaper option in the long run, as you avoid the risk of spiralling professional fees and penalties for non-compliance. It's simply a more financially sensible way to close the book on your dormant company.